It’s a question that a few people have asked me now, so I thought that I would get into the detail of what makes a good bank account for your matched betting and advantage play activities, and why you would choose one bank over another.

If you are new here, you may want to familiarise yourself with both Matched Betting and Advantage Play to get yourself up to speed.

What is the Best Bank Account for Matched Betting?

Put simply, you want a to choose a bank that does not have a high street presence. This means you want to take out an account with one of the new “challenger” banks such as Monzo or Starling who do not currently offer mortgages. You can also opt for simpler banks such as supermarket banks, or open an account with the Post Office as you are also much less likely to apply for a mortgage from one of these companies.

It is highly likely that when (I know this seems like a pipe dream to many of us!) you have enough money to put down a deposit on a house and apply for a mortgage it will be with one of the big high street banks.

For this reason, you don’t want to rule out the opportunity to apply with a particular bank because you’ve been putting all of your matched betting activity through them.

Why is Matched Betting a Problem for Mortgage Applications?

Probably the biggest issue is the fact that any income you make from matched betting or casino offers cannot be declared as income. An extra tax-free income is great, and for some people the money they make from both sports and casino offers is their full-time income.

However, because it is tax-free (and technically money earned from gambling) it cannot be counted towards your income on the application form. This means you will have to make sure your taxable income is large enough to cover the payments on the mortgage, which is impossible for people who do this full-time.

Then the essential part of getting approved is showing the bank manager your monthly income for the last 6-12 months through bank statements. Now if you’ve been matched betting the hell out of one of your accounts how is that going to look to an uninitiated bank manager?

He/She won’t be able to understand what you are doing and is most likely to think you are a problem gambler! What they are looking for is a stable, un-fluctuating income. This is why self-employed people sometimes struggle, because their income can vary one month to the next and so they often need to provide bank statements for up to 2 years.

Why Get a New Bank Account?

First of all, it’s important to set up a separate bank account in the first place. This will immensely improve your ability to track of all the ingoings and outgoings and tally up what you’ve made at the each of the month (you should be using Oddsmonkey’s Profit Tracker or an excel spreadsheet anyway to track this anyway).

You can then just transfer your profits back to your main current account, or even better keep the balance in there to accrue interest and re-invest back into back into matched betting.

The more money you can commit to matched betting and advantage play the more money you will make. The people who do this full-time initially re-invested everything they made until they had a pot of £5,000 – £10,000 and then started to take a wage from it.

That may seem like a lot of money and a long way off if you are just starting out, but I know people who have turned a £50 pot into £5,000 in the space of 6 months. Which makes my £500 to £5000 challenge seem a bit pathetic!

I take out some of my money each month to help to cover living expenses, so I don’t reinvest as much as I would like, and therefore my progress is a lot slower. I also have very little time to complete offers and so having a huge pot makes a lot less sense for me than it does for someone who does this full-time as I can only do 1-2 hours a day maximum.

Which Bank Should You Choose?

Now we’ve covered mortgages and why you need to set up a new account, it’s time to look at what your options are with regards to banks to use for your matched betting and advantage play activities.

You want to assess the ease of use, the benefits the account comes with, and what type of card is provided.

Challenger Banks

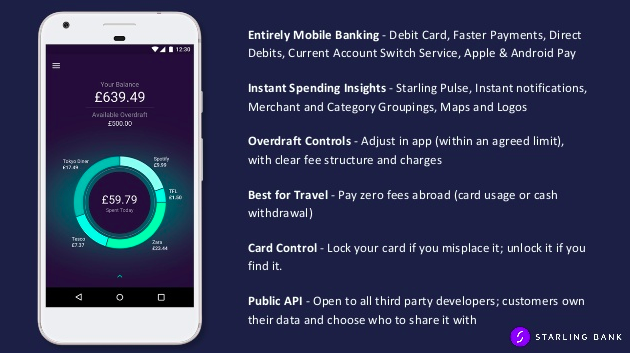

These banks are usually based on mobile apps alone, which makes managing your money a doddle. Just log in via your fingerprint on your phone and you can get in and immediately start managing your money.

The best thing about these accounts is the benefits. They offer competitive interest rates on current account balances but they also have the best functionality for travelling.

For both Starling and Monzo it is completely free to use your card abroad, with zero commission on transactions and cash withdrawals. Crucially they don’t give you a really poor exchange rate (with their commission rate secretly built in), they give you the exact market rate as it currently stands.

They also come with a proper Mastercard debit card. Many bookmakers and casinos will not accept pre-paid cards and so having a proper debit card is crucial. It also avoids any fees for depositing and withdrawing, which can be the case for pre-paid cards if accepted and e-wallets such as Paypal or Skrill.

In my experience the only bookmaker that doesn’t accept this type of card is Sky Bet which is annoying as it’s a biggie. But for the additional benefits I think it’s worth this slight inconvenience.

Ironically, before Sky gubbed me I only deposited/withdrew 4 times as I loaded it up with a big balance from my main account and pretty much survived from there onwards.

Simple current accounts from non-standard providers

Supermarkets often provide great current accounts and despite the fact that companies such as Tesco and Sainsburys offer mortgages, it is much more likely that your application will be with a traditional high-street lender.

The big advantage of these accounts come with a proper Visa debit card. Meaning it will be accepted across the board for bookmakers and casinos (remember casinos often charge a fee for deposits/withdrawals regardless of method).

However, the user experience is certainly much poorer. Speaking from personal experience (Tesco), their apps are usually poorly designed, slow and cumbersome. Which means going on the website via a browser on your laptop or PC to manage your money, often after completing about three security pages. When you’ve got very limited time to get through offers this becomes very annoying.

There of course will be the odd exception, but I haven’t got the time to sign up to multiple banks just to check how their tech performs.

They also don’t provide the additional benefits that challenger banks can, no special exchange rates, they charge fees for using your card abroad, and give poor returns from interest. If you aren’t bothered about these things then this type of account could be perfect for you.

Can I Not Just Go with a High Street Bank?

There may be some instances where you may want to just go with a normal high street bank. Perhaps mortgages are such a long way off for your personally that you don’t have to worry about your activity being presented to a bank manager.

If so, great!

It’s just then a case of deciding which bank has the best tech (NOT TSB!!!) and then assessing the benefits they offer (interest rates, cashback etc.) and picking the one that suits you the best. Once again speaking from personal experience I can highly recommend Natwest, I think their app is brilliant and I’ve never had any issues with them over the last 10 years.

Which Bank Account Do I Use For Matched Betting?

I personally use Starling. But since Monzo offer pretty much the same benefits I would recommend you to use either of them.

Yes, the Sky Bet thing was annoying initially, but since I’m now gubbed with all of their various offerings (Vegas, Casino etc.) it doesn’t affect me at all. It has also saves me tonnes of money abroad with no fees and great exchange rates. I used it for all of our transactions on the skiing holiday that was paid for by matched betting profits.

So there you have it. Hopefully you are a little bit wiser about making your decision on which bank to choose. If you enjoyed this article you may also want to read my guide on avoiding gubbings or how to make hundreds of pounds a month just from risk-free spins!